Over the past decades the world has experienced a process of financial integration and capital liberalisation that has permitted an increase in foreign capital accumulation, especially since the 1990s. Gross foreign assets and liabilities have become larger almost everywhere, but particularly in rich countries, and foreign wealth has reached around 2 times the size of the global GDP. The unequal distribution of this external wealth, with the top 20 % richest countries capturing more than 90% of total foreign wealth, poses constraints on the poorest countries.

Gastón Nievas and Alice Sodano investigate how rates of return on foreign assets and liabilities impacted different groups of countries across time. They put together a novel database encompassing the entire world (216 economies) for the period 1970-2022.

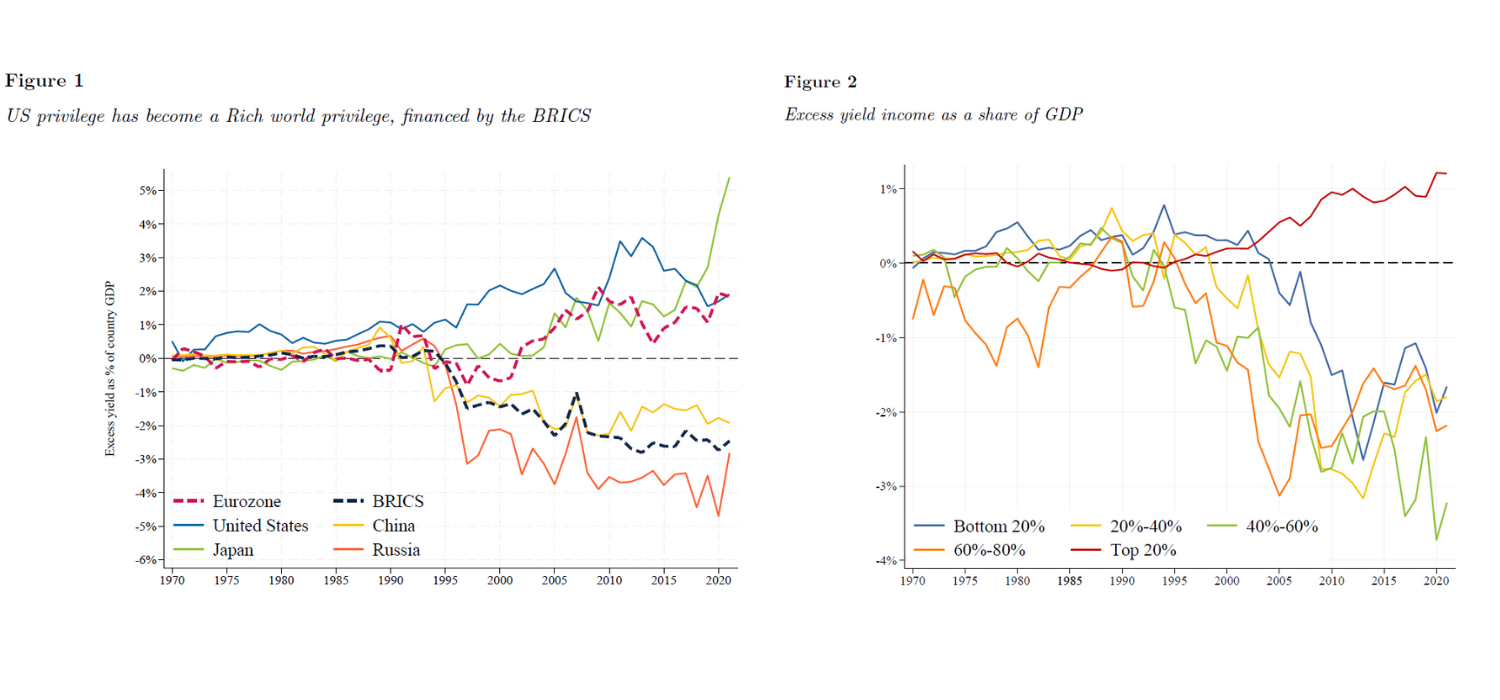

Key findings:

- Returns on foreign assets have decreased for everyone. On the contrary, returns on foreign liabilities have only decreased for the top 20% richest countries. This differential between returns on assets and returns on liabilities has extended the United States’ exorbitant privilege (rooted in the early years of the Bretton Woods system) into a rich world privilege.

- The richest countries have become the bankers of the world, attracting the excess savings by providing low-yield safe assets and investing these inflows in more profitable ventures. Such a privilege is translated in net income transfers from the poorest to the richest equivalent to 1% of the GDP of top 20% countries (and 2% of GDP for top 10% countries), alleviating the current account balance of the latter while deteriorating that of the bottom 80% by about 2-3% of their GDP.

- Moreover, rich countries also experience positive capital gains during the period, which further improves their international investment position.

- Contrary to prior beliefs, the positive return differential does not come from rich countries investing in riskier or more profitable assets. Instead, it is the result of rich countries accessing low interest debt, public and private, as a consequence of them being issuers of international reserve currencies.

- The paper proposes a set of policies that would overthrow such a privilege, including tax reform, a global reserve currency and a redesign of the governance of the international financial institutions.

Gastón Nievas, co-author of the paper, said:

“The size of net transfers that stem from the differential rates of return are substantial and are the result of unequal access to global capital markets. The burden they represent for poor countries cannot be neglected, each year they send 2-3% of their GDP to the rich world while they could be investing that amount in education, health or climate related policies. If we are aiming for a more egalitarian global system, we need to construct a more stable international monetary and financial system based on true democratic global governance. It’s imperative that developing countries have a voice and vote extending beyond major powers. Redefining the IMF quota formula is a crucial step toward promoting a more equitable international monetary and financial system.”

“The increasing divergence in development paths between rich economies, who are the dominant shareholders, and poorer economies, who are the primary clients, has reached alarming proportions. To stop labelling countries as privileged, rich, developed, developing, poor and so on, the international monetary and financial system need to be reformed, as they are currently unsustainable. We can reform them now or wait for another crisis to do so.”

AUTHORS

- Gastón Nievas, Paris School of Economics, World Inequality Lab

- Alice Sodano, Paris School of Economics, World Inequality Lab